Token Cap Table Allocation

Why Founders Are Misallocating Tokens to VCs?

Tokenomics is typically associated with a pie chart allocation that represents what % of tokens would be allocated across team, investors, treasury and community. The figures are typically determined by what would be considered acceptable based on benchmarks for non-investor token allocation and by bilateral negotiations between the team and the investors.

The token allocation gets challenging when a project that is raising capital for its equity entity is determining what % of tokens to offer to existing or future equity investors. There has yet been no framework to help guide founders determine what the accurate token allocation figure would be for a given or proposed equity cap table — leading to misallocation of token supply among the team and multiple classes of investors.

In this article we are going to cover:

- Value Accrual

- Value Only Accrues to Token Entity

- Value Accrues to Token Entity Owner by the Equity Entity

- Value Accrues to Token & Equity Entity

- Conclusion

Value Accrual

Before looking at the modeling side of things, let’s try to understand the relationship between the equity entity and the token entity. There are various models out there so far so let’s group them into categories:

- Value Accrues to Token Entity Only

- Value Accrues to Token Entity Owned by the Equity Entity

- Value Accrues to Both Token & Equity Entity

The key point here is value accrual; an entity is as valuable as the value accrued to it. Value is accrued to wherever the revenue is flowing to — any metric (transaction volume, user count) that represents future revenue could also be considered as a value driver as long as the future revenue that is converted by that metric (transaction volume, user count) would accrue to that entity.

If a game is charging 5% on secondary market transaction volume and that revenue is accruing to token holders, then token holders can collectively vote on how to spend those earnings. They can either decide to i) reinvest back into the protocol (marketing, hiring, new products, etc.), ii) distribute earnings to token holders (token buybacks, staking, etc.). Thus, the inherent fundamental value of the token is mainly driven by the value accrued through business fundamentals (revenue). And this value could accrue in the form of any currency (including the token issuer’s currency).

Similarly, if a decentralized exchange has $10bn daily volume but the exchange fees only accrue to the equity entity as revenue, then that decentralized exchange’s governance token has almost no fundamental value. Another example — that decentralized exchange has $10bn daily volume but there are no fees yet because the exchange enables free trading by subsidizing fees to incentivize growth. If the exchange decides that the future revenue that would be generated from exchange fees would only accrue to the equity entity, then the exchange’s governance token would again have no intrinsic value.

The core value driver of every token is the fundamentals of the underlying business — what % of the value accrues to the token entity vs the equity entity determines that token’s fundamental valuation.

The fundamental valuation methodology can get much more complex than this (as is the case with DCF) and there are many exceptions (asset-based valuation) but on a very high level, revenue = value accrual is a rule of thumb. In traditional financial markets (equity, bonds, commodities, FX), the majority of the invested capital is managed by institutional investors who are paid professionals to analyze securities and manage funds. Institutional investors build sophisticated models to value every tradable asset and come up with a valuation range that reflects the inherent fundamental value of a company based on their assumptions and the fear/greed mood of a given time range.

However, in crypto markets, the majority of the invested capital is managed by retail/degen investors who don’t give priority to fundamentals as much as the institutional investors — as is the case for Dogecoin, Shiba, Luna Classic, NFT PFPs. Thus, the market might not reflect the fundamentals as fast as the traditional finance markets but given more and more institutional capital is flowing into crypto, this is expected to change over the next 24–36 months.

1. Value Accrues to Token Entity Only

Let’s imagine a case where founders raise capital for the equity entity and plan to have a governance token that will be used to reward & incentivize active protocol participants. The governance token gives a sense of ownership to the active protocol participants with the aim of further strengthening those participants’ loyalty, retention and experience.

This could be a game that rewards the most-engaging players, a decentralized exchange or lending platform that rewards those that provide locked liquidity, a decentralized social network platform that rewards the most engaging content creators, a blockchain that rewards network validators. The token incentives could also be considered as a user acquisition/retention tool.

To encourage protocol participants that receive token rewards to hodl the tokens, the tokens should be designed in a way that they have some value driven by the future success of the business fundamentals. If all the protocol revenue is accruing to the equity entity instead of the token entity, then what drives the value of the token? Why would the active protocol participants hold these tokens instead of selling them immediately. Rational participants wouldn’t want to hold a token that has no additional utility than memecoins as they know the tokens would eventually be dumped.

This also leads to a bad reputation for the protocol as most crypto participants check the price of the protocol they use and perceive a constant drop in price as a sign of weakness or red flag. Given a token’s circulating supply will constantly increase to reward participants, if there is no demand-side utility to balance the growth in circulating supply, that token price will eventually drop.

Thus, the founders might consider accruing all the value to the token entity. This way, the token incentives given to participants will have a relatively higher $ value in addition to reflecting the future success of the protocol (giving the incentive receiving participants a rational reason not to sell) — converting users into loyal users, loyal users into evangelists.

However, if all the value created is accruing to the token entity, what drives the value of the equity entity? And more importantly — will equity investors’ stake become worthless? The equity entity will more or less be worthless (even though it still has legal power over the token entity) and to give flexibility value accrual & economy design flexibility to the developers, the equity investors should receive tokens in addition to their existing equity stake.

But what is the ideal % of tokens that existing equity investors should receive? If a pre-seed investor is getting 10% equity for a $1m investment (valuing the equity entity at $10m post-money), should they also get 10% of the token allocation?

No, they should get something smaller than 10%. Whether that is 8% or 5% or 3% will be based on the following assumptions;

i) Historical and Future Equity Cap Table Fundraising

ii) Treasury % of Token Allocation

iii) Community % of Token Allocation

iv) Token Public Sale

We built a model that calculates the implied token cap table allocation based on the assumptions listed above. The assumptions are colored in green in the spreadsheet and enable founders & investors to play around with the numbers to get a range of implied token cap table allocation figures. Click here to download the model.

Here’s a video that explains how to use the model, the rationale behind the calculation and how to think about the assumptions.

Why is it important to ensure the implied token cap table allocation matches the equity cap table? Any misallocation could lead to future problems & disappointments among team, investors and community. Founders and investors should have a framework and model to be well prepared for token allocation discussions. This model template aims to become a framework for future token cap table negotiations.

A fixed supply token cap table is different from an equity cap table. Whenever a team raises capital for an equity cap table, new shares are minted out of thin air — resulting in the dilution of existing shareholders. On the other hand, whenever a team raises capital for a token cap table, no new tokens are minted out of thin air — the tokens are given from the token protocol’s limited reserve.

2. Value Accrues to Token Entity Owned By The Equity Entity

Method 2 shares the same value accrual model as method 1 but the team portion of the tokens is fully owned by the equity entity. This is similar to the structural relationship between Sky Mavis and AXS tokens. Since value is directly accruing to the token entity rather than the equity entity, the rationale behind this method is that the equity entity derives its value from the ownership of its tokens. This aligns incentives between the token entity and the equity entity.

There are 2 ways to apply this model:

- Investors own both equity and tokens

- Investors own only equity (more on this in the next Vader Research article)

Investors Own Both Equity and Tokens

Investors own both equity (that drives its value from its token ownership) and tokens. The problem with this approach is that the investors are basically double dipping into tokens — having cumulative token ownership that is higher than their pro-rata equity ownership.

Let’s assume that the investors own 50% of the equity entity and the remaining shares are owned by the team.

Let’s also assume that the token cap table is allocated like the following table where investors own 20%. Keep in mind that the 20% team allocation goes to the equity entity rather than the founders & employees.

Assuming that the equity entity’s token holdings ($20m worth tokens) are distributed pro rata to equity shareholders (investors, founders, employees); the investors end up owning 30% of the token allocation (20% directly through token cap table and 10% indirectly through the equity cap table).

Thus, the team (founders & employees) ends up owning only 10% of the token allocation. Assuming that the value is accruing only to the token entity, this is a terrible deal for the team as they end up giving more tokens than they should have based on the equity cap table allocation.

Example

Sky Mavis & AXS token is one example where the value accrues to token that is owned by the equity entity but where the equity investors also get token allocation.

Early-stage VCs that invested in Sky Mavis got AXS token allocation — the team portion of 21% of AXS tokens went to the equity entity instead of going directly to the team. We don’t know the details of how the tokens owned by the equity entity were allocated but would be fair to assume that they were distributed pro-rata to equity entity shareholders.

Private sale investors only got 4% allocation — we don’t know the details of the investment structure. It is likely the VCs got a token allocation smaller than their pro-rata or maybe some VCs didn’t even get any allocation. Overall, this might not be a bad structure as long as it is well-balanced. In the case of Sky Mavis, the equity investors likely got access to allocation to future Sky Mavis tokens such as RON as well.

3. Value Accrues to Both Token & Equity Entity

In this case, the idea is to share the value accrual between the equity and the token entity. There are many varieties where this can be applied. The token capture a small portion of the overall value accrual or a large portion. It completely depends on the business model, product and industry.

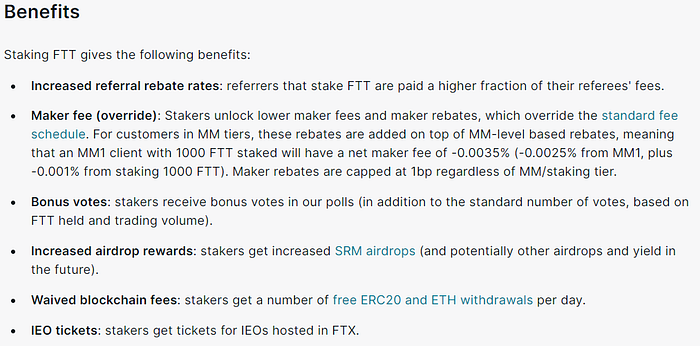

Let’s look at what centralized exchanges such as FTX and Binance use — owning FTT and BNB tokens give users a discount on the exchange trading fees. Thus, these tokens have an intrinsic value driven by the future success of the exchange business but unlike the first 2 models that we discuss, only a portion (determined by the developers) of the overall value accrues to the tokens.

Another method is what STEPN and Pegaxy does with their governance tokens. Both have economic models similar to Axie — a key difference is that in Axie, governance token AXS used to pay the breeding cost is automatically burnt. In other words, the value created from players paying $100 worth AXS to breed accrues to the AXS token holders as the circulating AXS supply gradually drops through breeding activity — leading to a lower circulating AXS supply and thus a higher AXS price.

Whereas in STEPN and Pegaxy, the governance token GMT and PGX used to pay the breeding cost isn’t automatically burnt and goes to the equity company as revenue. The developer can then make arbitrary decisions to burn some portion of the governance token revenue or conduct open market operations by buying the governance token on the open market to burn it. Assuming everything is equal, this makes the GMT and PGX tokens a less-attractive investment option from a fundamentals perspective as not 100% of the revenue is accruing.

Conclusion

This article focused on how a team that raised capital for an equity entity can decide on how to accrue value to the token entity in addition to what the ideal token allocation should be. There are other token cap table related topics such as what is the ideal treasury, community, liquidity pool, staking allocation in addition to the ideal vesting schedule.

In the next paper, we will be sharing a token cap table structuring & vesting proposal to enhance the long-term incentive alignment between VCs and the founders.

None of this is financial advice. If you want to learn more about Web3 Gaming, follow Vader Research on Twitter, YouTube and Spotify. If you want Vader Research to consult with your team on economy & token design, please fill in this form.