Yield Guild Games 101

The Virtual Land Baron of the Metaverse

Yield Guild Games aims to become the largest virtual land and NFT owner of the blockchain game metaverse. The YGG DAO is similar to a real estate investment company that builds a portfolio of properties and lends them out.

YGG is building a portfolio of game NFTs such as virtual lands, items, characters and leasing them out to “scholars” who can’t afford to buy those NFTs. It costs $1–2k to buy 3 Axies in order to play Axie Infinity where one can earn $10–20 a day.

Business Model

YGG earned $330k in July; all in the form of SLPs earned by Axie Infinity scholars. YGG’s earnings are driven by a)NFT count, b)scholar count, c)IRR.

a)NFTs: To increase earnings, YGG has to purchase more NFTs and rent them out. YGG currently has $10m worth NFTs and has $900m in liquid tokens in the treasury that can be used to buy NFTs. Future earnings can also be used to buy NFTs.

b)Scholars: Having a large, vibrant community of scholars and scholar candidates is crucial for YGG’s long-term success. This increases asset efficiency by ensuring there’s constant demand for YGG’s NFTs.

YGG’s user acquisition strategy is driven by community managers who are responsible for recruiting, onboarding, training new scholars in exchange for 20% of the scholar’s earnings. Scholars are chosen by community managers who are chosen by YGG core members. There are currently no hard KPI requirements on scholar or manager performance which could lead manager/scholar hiring decisions to be based on nepotism.

There are currently 5k YGG scholars whereas the growth potential for YGG scholars is massive as there are 2 billion mobile game players and 4 billion smartphone owners in the world.

c)IRR: IRR is driven by the average NFT quality and the average scholar performance. High-quality NFTs and better performing scholars lead to higher IRR. IRR on NFTs was 300% in July.

YGG’s niche play-to-earn community makes it a great user acquisition channel for upcoming blockchain games that can offer rare, high-quality NFTs in exchange for YGG incentivizing its community to play those games. This makes YGG the ultimate king-maker. 45% of YGG tokens will be distributed to the community managers and scholars.

Treasury

13% of YGG tokens were distributed to the YGG treasury. The YGG treasury owns $10m worth NFTs and $1bn worth liquid tokens ($800m YGG, $17m AXS, $16m USDC). Thus, YGG can buy a further $1bn+ worth NFTs.

Although 100% of earnings and 80% of NFTs are currently exposed to Axie Infinity, only 3% of the YGG treasury assets are exposed to Axie Infinity. This busts the myth that YGG’s performance is dependent on Axie Infinity.

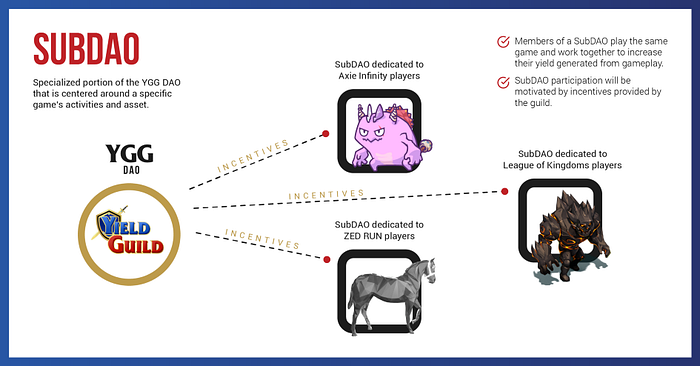

SubDAOs

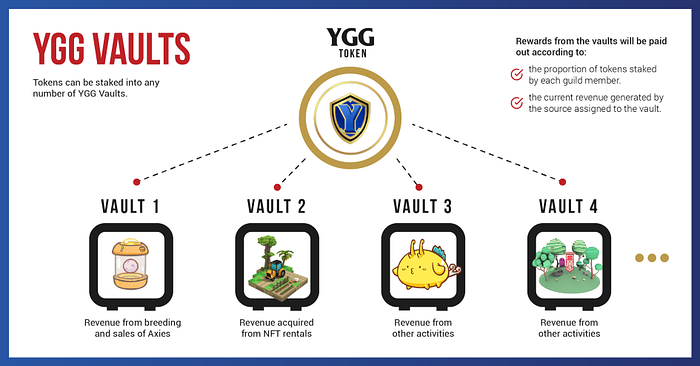

YGG will own NFTs for multiple games and each game will yield a different IRR whereas YGG owners who stake will receive a diversified index of yield from all games.

SubDAOs allow YGG holders to bet on a specific game; if one believes that League of Kingdom NFTs will generate the highest IRR, one can stake YGG tokens in the League of Kingdom subDAO vault and solely receive yield from the Leauge of Kingdom scholar earnings.

Each subDAO will have its own DAO and token as a subsidiary to the master YGG DAO and YGG token. This approach gives YGG holders the option to bet on an individual game and YGG community managers the flexibility to distribute respective incentive tokens.

SubDAO token holders can vote on how to use the treasury proceedings, which NFTs to buy and which community managers to recruit. NFT and game investment decisions are currently made by the core YGG members.

Future Potential

YGG’s textbook valuation can be driven by NFTs, liquid tokens, current earnings and its community -> P/BV, P/E, P/Users. But I believe YGG should be treated as an early-stage startup and shouldn’t be valued simply by current SLP earnings as the potential for growth is huge. In 1996, one could have valued Amazon on its current book sales or on its future potential as a dominant e-commerce platform.

Michiko_0x posted a great tweet thread about applying July IRR to treasury assets and came up with a P/E ratio. The problem with this approach is that the IRR assumption is entirely driven by SLP earnings in July. I expect IRR from Axies to go down due to various issues around Axie Infinity’s sustainability.

There are 3 cases that make YGG a good investment:

i)YGG as an index of blockchain game NFTs -> As various blockchain games grow their user base; YGG’s NFTs will generate more yield from lending to scholars and will gain in value. Therefore, YGG is a bet on the growth of the blockchain game sector as a whole.

ii)YGG as a blockchain game VC -> Axie Infinity generated more than 1000x to its seed investors in less than 2 years. YGG’s king-maker strategic positioning gives it access to invest in most blockchain games at favourable valuations. YGG can generate substantial returns from its VC investments.

iii)YGG as a rental marketplace for game NFTs -> YGG can currently only rent its own NFTs which restricts scholar growth. There are many Axie owners who bought Axies as investments and are looking for scholars. YGG can become a Zillow-like rental marketplace for game NFT owners and scholars. This can even be expanded to non-game NFTs (Cryptopunks, etc,) although there are existing competitors such as Scalar Capital-backed reNFT.

Conclusion

YGG is a diversified, picks and shovels play on the long-term success of blockchain games. I’m grateful to the Yield Guild Games core team and discord members who have diligently answered all my questions. If you want to learn more about DeFi and blockchain games, you can follow me on Twitter.

Disclosure: I hold a small portion of YGG tokens.